Title

THE A REPORT

2025 H2

Jiwon JUNG

Researcher

Jiwon JUNG

ResearcherKorean Film Council (KOFIC)

Updated on 12 May 2026

Overview:

Recovery Led by Foreign Titles, Structural Risks Remain

In 2025, the Korean film industry entered a phase where partial recovery coexists with deeper structural pressure. In the first half of the year, market conditions remained subdued. Total box office revenue reached KRW 407.9 billion with 42.5 million admissions, and most major releases failed to surpass the 3 million threshold. As a result, investment, planning, and production activities slowed across the board, and industry sentiment became increasingly cautious.

Conditions began to improve after the introduction of cinema ticket discount policies in July. The summer peak season saw a rebound in admissions, supported by renewed audience demand. In the second half of the year, several large-scale foreign titles—including Zootopia 2, Demon Slayer: Kimetsu no Yaiba - Infinity Castle, and F1: The Movie—played a key role in driving box office recovery. Annual revenue reached approximately KRW 1.047 trillion, with total admissions of 106.09 million, suggesting a return to a more stable level compared to the immediate post-pandemic period.

However, this recovery was not evenly distributed. Box office performance relied heavily on foreign films, while Korean films faced declining market share and weaker profitability. At the same time, structural adjustments became more visible. Major distributors reduced new investment, and production activity increasingly concentrated on mid- and low-budget projects. Policy discussions also intensified, particularly around the inclusion of OTT content within regulatory frameworks and the possible institutionalization of holdback rules.

Taken together, the industry is showing signs of short-term stabilization, but underlying risks remain. Investment decisions continue to be made cautiously, reflecting uncertainty about future demand. At the same time, there is a growing expectation that public policy and financial support will play a more active role in stabilizing the production and distribution ecosystem.

Top 10 Films in Korean Box Office (2025)

You can scroll left and right to view the content.

| No | Title | Director | Country | Genre | Gross (KRW) |

Gross (USD) |

Production Company |

Distribution Company |

|---|---|---|---|---|---|---|---|---|

| 1 | Zootopia | Jared Bush, Byron Howard | USA | Animation | 74.12B | 52.12M | Walt Disney Animation Studios | The Walt Disney Co. Korea |

| 2 | Demon Slayer: Kimetsu no Yaiba - Infinity Castle | Haruo Sotozaki | Japan | Animation | 61.32B | 43.12M | Ufotable | CJ ENM Corp. |

| 3 | F1: The Movie | Joseph Kosinski | USA | Action | 54.94B | 38.63M | Apple Studios, Jerry Bruckheimer Films, Plan B Entertainment | Warner Bros. Korea |

| 4 | My Daughter is a Zombie | Pil Gam-Seong | Korea | Comedy, Drama | 53.13B | 37.36M | STUDIO N | Next Entertainment World |

| 5 | Avatar: Fire and Ash | James Cameron | USA | Sci-Fi, Action | 52.41B | 36.85M | Lightstorm Entertainment | The Walt Disney Co. Korea |

| 6 | Chainsaw Man - The Movie: Reze Arc | Tatsuya Yoshihara | Japan | Animation | 36.07B | 25.36M | MAPPA | Sony Pictures |

| 7 | Mission: Impossible - The Final Reckoning | Christopher McQuarrie | USA | Action | 33.26B | 23.38M | Paramount Pictures, Skydance, TC Productions | Lotte Entertainment |

| 8 | Yadang: The Snitch | Hwang Byeong-Gug | Korea | Crime, Action | 32.00B | 22.50M | Hive Media Corp. | Plus M Entertainment |

| 9 | Mickey 17 | Bong Joon-Ho | USA | Adventure, Sci-Fi | 29.71B | 20.89M | Plan B Entertainment | Warner Bros. Korea |

| 10 | No Other Choice | Park Chanwook | Korea | Thriller, Comedy | 28.77B | 20.23M | Moho Film, CJ ENM STUDIOS | CJ ENM Corp. |

Top 10 Domestic Films in Korean Box Office (2025)

You can scroll left and right to view the content.

| No | Title | Director | Country | Genre | Gross (KRW) |

Gross (USD) |

Production Company |

Distribution Company |

|---|---|---|---|---|---|---|---|---|

| 1 | My Daughter is a Zombie | Pil Gam-Seong | Korea | Comedy, Drama | 53.13B | 37.36M | STUDIO N | Next Entertainment World |

| 2 | Yadang: The Snitch | Hwang Byeong-Gug | Korea | Crime, Action | 32.00B | 22.50M | Hive Media Corp. | Plus M Entertainment |

| 3 | No Other Choice | Park Chanwook | Korea | Thriller, Comedy | 28.77B | 20.23M | Moho Film, CJ ENM STUDIOS | CJ ENM Corp. |

| 4 | Hitman2 | Choi Won-Sub | Korea | Comedy | 23.98B | 16.86M | Very Good Studio, Studio Target | BY4M Studio |

| 5 | Boss | Ra Hee-Chan | Korea | Comedy | 23.39B | 16.45M | Hive Media Corp. | Hive Media Corp., MINDMARK Inc. |

| 6 | Harbin | Woo Min-Ho | Korea | Drama | 20.73B | 14.58M | Hive Media Corp. | CJ ENM |

| 7 | The Match | Kim Hyung-Ju | Korea | Drama | 20.04B | 14.09M | Moonlight Film | BY4M Studio |

| 8 | Hi-Five | Kang Hyung-Chul | Korea | Comedy | 17.55B | 12.34M | Annapurna Films | Next Entertainment World |

| 9 | Noise | Kim Soo-Jin | Korea | Horror | 16.76B | 11.78M | Finecut Co., Ltd. | BY4M STUDIO |

| 10 | Dark Nuns | Kwon Hyeok-Jae | Korea | Mystery | 16.13B | 11.34M | Zip Cinema | Next Entertainment World |

Box Office Revenue and Admission Figures (2017-2025)

You can scroll left and right to view the content.

| Category | Segment | 2017–2019 Avg. | 2024 | 2025 | Change vs 2024 (%) |

Change vs 2017–2019 Avg. (%) |

|---|---|---|---|---|---|---|

| Box Office Revenue (KRW billion) |

Total | 1,828 | 1,195 | 1,047 | -12.4% | -42.7% |

| Korean Films | 929 | 691 | 419 | -39.4% | -54.9% | |

| Foreign Films | 899 | 504 | 628 | +24.7% | -30.2% | |

| Admissions (1,000) |

Total | 220,980 | 123,130 | 106,090 | -13.8% | -52.0% |

| Korean Films | 113,230 | 71,470 | 43,580 | -39.0% | -61.5% | |

| Foreign Films | 107,750 | 51,650 | 62,510 | +21.0% | -42.0% |

Production Landscape:

Animation Dominance and Mid-Budget Stability

In 2025, the Korean film production landscape was shaped by both genre diversification and the continued importance of mid-scale commercial films. The structure in which large commercial projects and independent or art-house films coexist remained largely unchanged, but the balance within this structure showed notable shifts.

By genre, animation recorded the highest revenue share, with 103 titles accounting for 26.9% of total box office revenue. Drama followed with 233 titles (15.1%), while comedy (31 titles, 12.7%) and action (60 titles, 10.9%) trailed behind. In particular, global animation titles such as Zootopia 2 and Demon Slayer: Kimetsu no Yaiba - Infinity Castle ranked among the top-grossing films of the year, reinforcing the sustained strength of animation in the post-pandemic market.

Demon Slayer: Kimetsu no Yaiba - Infinity Castle © CJ ENM Corp.

– Among foreign films, animation titles performed strongly worldwide and led the 2025 box office.

Within Korean productions, comedy emerged as a relatively stable genre. Mid-budget films such as My Daughter is a Zombie, Hitman 2, and Boss achieved meaningful box office results, contributing to a total comedy revenue of approximately KRW 130 billion. By contrast, the action genre, which had dominated from 2021 to 2024, declined to fourth place, indicating a shift in audience preference and genre performance.

Hitman 2 © BY4M Studio

Boss © Hive Media Corp.

– Among Korean films, mid-budget comedy titles performed well at the box office.

From an industry structure perspective, major investor-distributors—including CJ ENM, Lotte Entertainment, Next Entertainment World, Showbox, and Plus M—continue to anchor commercial film production. At the same time, a wide range of independent production companies remain active in smaller-scale projects, maintaining diversity within the ecosystem. In post-production, companies such as Dexter Studios have expanded their capabilities, particularly in VFX, and are increasingly participating in international projects.

A notable policy development is the expansion of support for mid-budget Korean films by the Korean Film Council. The program provides partial production funding for theatrical features that meet certain budget criteria. As of 2026, the total scale of the program has expanded to approximately KRW 20 billion, with up to KRW 2 billion allocated per project. The scheme is designed to operate in combination with private investment, helping to fill the gap between large-scale blockbusters and low-budget productions.

Despite these efforts, rising production costs and declining audience numbers have led to more cautious investment behavior. As a result, production companies are increasingly pursuing risk diversification strategies, including collaboration with global OTT platforms, international co-productions, and the development of content based on established intellectual property. In this context, the production landscape is gradually adjusting toward a more risk-managed and diversified structure.

Financing Models:

Conservative Investment and Expanded Public Support

In 2025, the financing structure of the Korean film industry continued to rely on investor-distributors and investment funds, but overall investment behavior became more selective. Market participants increasingly prioritized risk control over expansion.

The number of Korean commercial films with production budgets above KRW 3 billion declined to 31, representing a decrease of six compared to the previous year. At the same time, the average return fell to –33.1%, reflecting continued pressure on profitability. While the traditional model—reinvesting box office returns into new projects—remains in place, uncertainty in audience demand and rising production costs have led to more cautious capital allocation.

Investment is now concentrated on mid-budget projects in the KRW 3–6 billion range, as well as genres with relatively predictable performance. Projects based on existing IP or established fan bases are also receiving greater attention. Additional financing sources such as streaming pre-sales, international distribution deals, and co-productions are being used to complement core funding, but private investment continues to play a central role in the overall structure.

In response to these conditions, public support mechanisms are being strengthened. The Korean Film Council has continued to expand its support for development-stage projects, including planning, adaptation, and scriptwriting. Eligibility criteria have also been broadened to include experience in OTT content production, reflecting changes in the industry environment. In 2025, total funding for the writer category increased to KRW 760 million, and new programs targeting mid-budget films were introduced.

Looking ahead, government-backed financing is expected to play a larger role. In 2026, the government increased its contribution to the film account of the Fund of Funds to KRW 49 billion, with the goal of establishing funds totaling KRW 81.8 billion. This includes a main investment fund, a mid- and low-budget fund, and a dedicated animation fund. The government’s contribution ratio has also been raised to 60%, reducing the burden on private investors and encouraging fund formation.

Tax incentives remain an important complementary tool. Production cost tax credits are in place until the end of 2028 and apply to both theatrical and OTT content. Recent tax revisions also expand incentives for investment in cultural industry funds, supporting indirect investment channels.

Taken together, the current financing environment reflects a shift toward stabilization rather than growth. Private investment remains cautious, while public funding is being used to support key segments of the market. This mixed financing structure is likely to remain a defining feature in the near term.

Distribution Climate:

Foreign Film Share Expansion and Premium Strategy

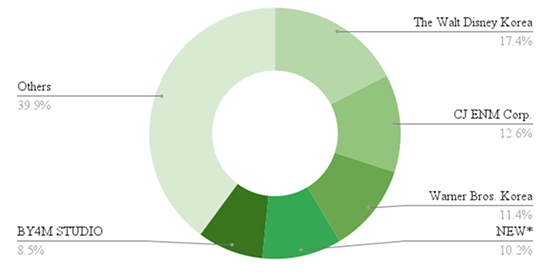

In 2025, the Korean film distribution market continued to be structured around major investor-distributors, while the role of foreign films expanded further. By total box office revenue, Korean films recorded approximately KRW 419.1 billion, whereas foreign films reached around KRW 627.9 billion. This indicates that foreign titles accounted for approximately 60% of the overall market, continuing a trend that has persisted since the pandemic period.

This imbalance is also visible in box office rankings. Among Korean films, My Daughter is a Zombie distributed by Next Entertainment World recorded the highest performance with approximately 5.63 million admissions. Other notable titles included Yadang: The Snitch (Plus M), No Other Choice (CJ ENM), and Hitman 2 (BY4M). However, foreign films dominated the top positions. Zootopia 2 led the annual box office with around 7.7 million admissions, followed by Demon Slayer: Kimetsu no Yaiba - Infinity Castle and F1: The Movie, all of which maintained strong audience demand throughout their runs.

Figure of Market Share by countries (2025)

Source: korean Film Council, 2025 Korean Film Industry Report

Note: Market share is based on total annual box office revenue and not on the number of titles<

Note: Market share is based on total annual box office revenue and not on the number of titles<

Figure of Released Domestic Films (2025)

Source: korean Film Council, 2025 Korean Film Industry Report

From a structural perspective, the distribution system remains vertically integrated. Major companies continue to handle investment, production, and distribution simultaneously, often in close coordination with multiplex chains. This structure allows for relatively stable supply and scheduling control. At the same time, global studios such as Disney, Warner Bros., and Sony are actively distributing films directly in Korea, increasing their influence in the local market.

Changes are also visible in distribution strategies. Imports of specific genres, particularly Japanese animation, have increased. In addition, premium screening formats such as IMAX and 4DX are playing a more important role in maximizing box office returns. In 2025, premium screenings accounted for 16.1% of foreign film revenue, up by 5.2 percentage points compared to the previous year.

In this context, the distribution environment can be understood as a hybrid structure, where domestic distributors maintain operational control while global studios and premium formats increasingly shape market performance.

Top 5 Distributors' Market Share (2025)

Source: korean Film Council, 2025 Korean Film Industry Report

* Next Entertainment World

Note: Market share is based on total annual box office revenue and not on the number of titles.

* Next Entertainment World

Note: Market share is based on total annual box office revenue and not on the number of titles.

Theatrical Reach:

Structural Downsizing and Experience-Oriented Strategy

In 2025, the theatrical exhibition sector continued to adjust following the pandemic, showing both a reduction in infrastructure and a shift toward higher-value viewing experiences.

By the end of the year, the number of cinemas declined to 547, down 4.0% year-on-year. The number of screens fell to 3,154 (−4.3%), while total seating capacity decreased to approximately 407,000 (−7.1%). Notably, seating capacity has declined for four consecutive years, indicating an ongoing structural contraction in the exhibition sector.

Regional distribution shows a similar pattern. Gyeonggi Province recorded the highest number of cinemas (131), followed by Seoul (86), while Sejong had the smallest number at three. Cinema numbers declined even in major regions such as Gyeonggi and Seoul, reflecting a nationwide trend. The number of screens per 100,000 people also decreased slightly.

At the same time, ticket pricing trends provide additional insight into market conditions. The average ticket price in 2025 was KRW 9,869, up 1.7% from the previous year. After exceeding KRW 10,000 for the first time in 2022, the average price declined for two consecutive years—KRW 10,080 in 2023 and KRW 9,702 in 2024—before recovering slightly in 2025.

It should be noted that the “average ticket price” used in industry statistics is calculated by dividing total box office revenue by total admissions. As such, it reflects the effective price paid by audiences after discounts and promotions, rather than the official listed ticket price.

The earlier decline in the average ticket price is generally attributed to expanded discount promotions, which lowered the effective price paid by audiences. In contrast, the increase in 2025 reflects changes in revenue composition. While premium-format screenings declined in 2024 due to weaker performance of foreign films, premium screening revenue increased by 46.3% in 2025, contributing to a modest rise in the average ticket price.

For Korean films, the average ticket price declined slightly to KRW 9,617, down 0.5% year-on-year. After exceeding KRW 10,000 in 2022, the average ticket price for Korean films has decreased for three consecutive years, indicating continued pricing pressure in the domestic segment.

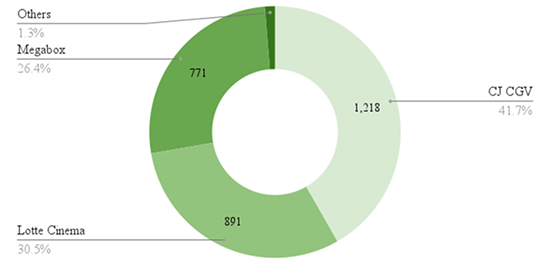

Top 3 Cinema Chains in Korea (2025)

Source: korean Film Council, 2025 Korean Film Industry Report

Average Ticket Price (2021–2025)

| Category | 2021 | 2022 | 2023 | 2024 | 2025 |

|---|---|---|---|---|---|

| Revenue (KRW billion) | 585 | 1,160 | 1,261 | 1,195 | 1,047 |

| Admissions (1,000) | 60,530 | 112,810 | 125,140 | 123,130 | 106,090 |

| Avg Ticket Price - Total (KRW) | 9,656 | 10,285 | 10,080 | 9,702 | 9,869 |

| Avg Ticket Price - Korean Films (KRW) | 9,518 | 10,049 | 9,850 | 9,667 | 9,617 |

| Avg Ticket Price - Foreign Films (KRW) | 9,716 | 10,582 | 10,297 | 9,749 | 10,045 |

Note: Average ticket price = total box office revenue ÷ total admissions

Despite these pricing dynamics, the overall exhibition structure remains highly concentrated. The three major multiplex chains—CJ CGV, Lotte Cinema, and Megabox—account for the majority of screens and revenue, although they are also reducing their scale.

At the same time, exhibitors are strengthening premium offerings to attract audiences. Formats such as IMAX, ScreenX, and Dolby Cinema, along with upgraded seating, are expanding. These efforts suggest a continued focus on enhancing the theatrical experience as a way to respond to structural challenges.

In this context, the theatrical sector is evolving through a combination of structural adjustment and experience differentiation, rather than simple volume recovery.

Technology and Production Services:

Integration of AI Across the Production Pipeline

The technology and production services sector in the Korean film industry is evolving from a post-production-centered model toward a more integrated role across the entire production process. This shift is becoming more pronounced around 2026, particularly with the adoption of AI and virtual production technologies.

Policy support has played a key role in this transition. The Korean Film Council has introduced AI-based production support programs that cover both feature-length and short-form content. In the feature category, a total of KRW 1.6 billion is allocated to support around eight projects, with KRW 200–300 million per project. A minimum self-financing requirement of 10% is applied, encouraging participation from production companies with a certain level of capacity and commercial intent.

In the short film category, KRW 600 million supports approximately 30 projects, with up to KRW 20 million per project. Unlike the feature category, individual creators are eligible to apply. A notable condition is the requirement to use generative AI in all or a significant portion of the production process, effectively positioning AI as a core production tool rather than an optional element.

The scope of funding covers the entire production pipeline, including AI tools, pre-production, filming, and post-production stages. This structure encourages the practical integration of AI into real production workflows.

In the industry, AI applications are already expanding across multiple stages. These include storyboarding, pre-visualization, concept design, editing assistance, dubbing, subtitle generation, and marketing content creation. At the same time, virtual production technologies, such as LED stage environments, are becoming more widely adopted, enabling hybrid production models that combine physical and digital elements.

In this context, the Korean film industry appears to be entering an early stage of transition toward a technology-driven production system, with AI and virtual production positioned as key drivers of change.

Streaming Platforms and Digital Growth:

Platform Competition and Market Rebalancing

In 2025, the non-theatrical market for Korean films continued to shift toward an OTT-centered structure, while the traditional VOD market experienced further contraction.

According to industry data, TV VOD revenue declined to KRW 138.1 billion, down 18.7% compared to the previous year, marking three consecutive years of decline. This trend reflects both reduced theatrical performance and a decrease in the number of Korean film releases, as well as the growing substitution effect of OTT platforms.

Changes are also evident in subscription patterns. According to the latest official data available as of 2026, released by the Ministry of Science and ICT in November 2025, IPTV subscriptions increased slightly to 21.41 million households, while digital cable TV subscriptions declined to 12.09 million. This suggests a gradual but consistent shift from traditional pay-TV to OTT-based consumption.

Competition among OTT platforms has intensified. Netflix continues to maintain the largest user base and viewing share, while domestic platforms are pursuing growth through partnerships and bundled offerings. For example, TVING has expanded bundled subscription models through partnerships with telecom operators and digital services, while TVING and Wavve have introduced joint subscription products. In 2025, a “3PACK” bundle combining TVING, Wavve, and Disney+ was also launched, reflecting increased collaboration among platforms.

Content strategies are also evolving. Investment in high-cost original Korean content has slowed since 2022, with platforms shifting toward more cost-efficient formats such as sports broadcasting, live content, and entertainment programming. At the same time, international co-productions, particularly with Japan, are increasing, reflecting a stronger focus on global distribution.

From a consumption perspective, performance differences between theatrical and digital markets have become more noticeable. Some Korean films perform relatively better in the home viewing market than in theaters, while others show the opposite pattern. This indicates that box office success and digital performance are not always directly correlated.

Overall, the digital market is undergoing a process of rebalancing, with OTT platforms strengthening their position through both competition and collaboration.

Top 5 Streamers (December 2025)

| Rank | Name | Monthly Active Reach |

Subscription Fee Range |

|---|---|---|---|

| 1 | Netflix | 15.16M | USD 5.2–12.6 |

| 2 | Coupang Play | 8.53M | USD 5.8–7.3 |

| 3 | TVING | 5.25M | USD 4.2–12.6 |

| 4 | Disney+ | 2.39M | USD 7.3–10.3 |

| 5 | Wavve | 2.35M | USD 5.9–10.3 |

Source: Wiseapp·Retail, Jan. 13, 2026, “Netflix Hits Record-High App Users!...OTT App Rankings?”

Note:

- As major streaming platforms do not disclose exact subscriber counts, Monthly Active Users (MAU) are used as a proxy. MAU figures may fluctuate due to industry factors, including sports league off-seasons, major content release cycles, and changes in promotional or partnership strategies aimed at improving profitability.

- The pricing plans of OTT platforms may vary depending on each company's specific package composition. (e.g., ad-supported, premium, etc.)

Note:

- As major streaming platforms do not disclose exact subscriber counts, Monthly Active Users (MAU) are used as a proxy. MAU figures may fluctuate due to industry factors, including sports league off-seasons, major content release cycles, and changes in promotional or partnership strategies aimed at improving profitability.

- The pricing plans of OTT platforms may vary depending on each company's specific package composition. (e.g., ad-supported, premium, etc.)

International Co-Production:

Expanding Export Base and Production Collaboration

In 2025, the international activities of the Korean film industry showed growth in both exports and collaborative production.

Total overseas sales of Korean films reached approximately USD 92.63 million, representing a 7.6% increase year-on-year. Exports of completed films totaled USD 50.28 million, up 19.9%, while new project contracts accounted for USD 46.16 million, playing a key role in driving overall growth.

By region, Asia remained the largest market, accounting for 63.7% of total exports, followed by Europe at 16.8%. Japan and Taiwan continued to serve as major markets, while Indonesia showed notable growth, ranking third with approximately USD 3.07 million in imports. Vietnam and China also remained important export destinations, indicating that the overseas market for Korean films continues to expand, particularly within Asia.

In terms of collaboration, international co-productions and overseas filming projects are becoming more active. Joint productions involving countries such as the United States, India, Japan, and Mongolia are underway, reflecting a diversification of partnerships. At the same time, global OTT productions are increasingly choosing Korea as a filming location, further strengthening links between international content producers and local production infrastructure.

Location services also remain a key area of international cooperation. In 2025, total spending by foreign productions in Korea reached approximately USD 42.34 million. Although this represents a slight decrease from the previous year, production teams from multiple countries continue to select Korea as a filming destination.

In summary, the Korean film industry is expanding its global presence not only through content exports but also through production services and collaborative projects, positioning itself as an active participant in the international production network.

Jiwon JUNG

Researcher, Korean Film Council (KOFIC)

Working at the KOFIC since 2020, focusing on film policy development and industry analysis. Since 2023, leading research on the annual Korean Film Industry Report with emphasis on box office statistics and market trends.

Note: Exchange rates are based on the annual average basic exchange rate published by the Bank of Korea.

(2025: USD 1 = KRW 1,422.22)