Title

THE A REPORT

2025 H2

Nyay BHUSHAN

Producer, Photographer

Nyay BHUSHAN

Producer, Photographer

Updated on 12 May 2026

Overview

Record year at the box office

Looking at industry data for 2025, one can safely assume that Indian cinema is on a growth path though headwinds remain. According to the annual box office analysis by Ormax Media, 2025 was the first time that total gross box office collections touched an all-time high of INR 133.87 billion (USD 1.53 billion), surpassing the record set in 2023 at INR 122.26 billion (USD 1.40 billion).

As for a reality check, while box office revenues may appear on a growth curve, footfalls declined by 6% to 832 million in 2025 from 883 million in 2024, largely due to the rise in average ticket prices which increased by 20% to INR 161 (USD 1.84) in 2025 from INR 134 (USD 1.53) in 2024.

Add to this the fact that India remains heavily under-screened and that gives a sense of the massive potential that continues to remain untapped when it comes to monetising theatrical revenues.

Top 10 Films in Indian Box Office (2025)

You can scroll left and right to view the content.

| No. | Title | Director | Country | Genre | Gross (INR) |

Gross (USD) |

Production Company |

Distribution Company |

|---|---|---|---|---|---|---|---|---|

| 1 | Dhurandhar (Stalwart) | Aditya Dhar | India | Action, Thriller | 9.5B | 108.57M | Jio Studios & B62 Studios | Jio Studios |

| 2 | Kantara: Chapter 1 (Mysterious Forest) | Rishab Shetty | India | Adventure, Drama | 7.24B | 82.74M | Hombale Films | AA Films, Hombale Films |

| 3 | Chhaava (Cub) | Laxman Utekar | India | Historical Epic | 6.93B | 79.20M | Maddock Films | Pen Marudhar |

| 4 | Saiyaara (Wandering Star) | Mohit Suri | India | Romantic Drama | 3.96B | 45.26M | Yash Raj Films | Yash Raj Films |

| 5 | Coolie (Porter) | Lokesh Kanagaraj | India | Action, Thriller | 3.25B | 37.14M | Sun Pictures | Red Giant Movies |

| 6 | Mahavatar Narsimha (The Great Incarnation Narsimha) | Ashwin Kumar | India | Animation, Myth | 3.01B | 34.40M | Kleem, Hombale Films | AA Films, Hombale films, Geetha Arts |

| 7 | War 2 | Ayan Mukerji | India | Action | 2.83B | 32.34M | Yash Raj Films | Yash Raj Films |

| 8 | Avatar: Fire and Ash | James Cameron | USA | Sci-Fi, Action | 2.39B | 27.31M | 20th Century Studios, Lightstorm Entertainment |

Disney Star India |

| 9 | They Call Him OG | Sujeeth | India | Action, Thriller | 2.24B | 25.60M | DVV Ent. | DVV Ent. |

| 10 | Sankranthiki Vasthunam (Coming for Sankranthiki) | Anil Ravipudi | India | Action, Comedy | 2.22B | 25.37M | Sri Venkateswara Creations | Sri Venkateswara Creations, Sony Pictures India |

Top 10 Domestic Films in Indian Box Office (2025)

You can scroll left and right to view the content.

| No. | Title | Director | Country | Genre | Gross (INR) |

Gross (USD) |

Production Company |

Distribution Company |

|---|---|---|---|---|---|---|---|---|

| 1 | Dhurandhar (Stalwart) | Aditya Dhar | India | Action, Thriller | 9.5B | 108.57M | Jio Studios & B62 Studios | Jio Studios |

| 2 | Kantara: Chapter 1 (Mysterious Forest) | Rishab Shetty | India | Adventure, Drama | 7.24B | 82.74M | Hombale Films | AA Films, Hombale Films |

| 3 | Chhaava (Cub) | Laxman Utekar | India | Historical Epic | 6.93B | 79.20M | Maddock Films | Pen Marudhar |

| 4 | Saiyaara (Wandering Star) | Mohit Suri | India | Romantic Drama | 3.96B | 45.26M | Yash Raj Films | Yash Raj Films |

| 5 | Coolie (Porter) | Lokesh Kanagaraj | India | Action, Thriller | 3.25B | 37.14M | Sun Pictures | Red Giant Movies |

| 6 | Mahavatar Narsimha (The Great Incarnation Narsimha) | Ashwin Kumar | India | Animation, Myth | 3.01B | 34.40M | Kleem, Hombale Films | AA Films, Hombale films, Geetha Arts |

| 7 | War 2 | Ayan Mukerji | India | Action | 2.83B | 32.34M | Yash Raj Films | Yash Raj Films |

| 8 | They Call Him OG | Sujeeth | India | Action, Thriller | 2.24B | 25.60M | DVV Ent. | DVV Ent. |

| 9 | Sankranthiki Vasthunam (Coming for Sankranthiki) | Anil Ravipudi | India | Action, Comedy | 2.22B | 25.37M | Sri Venkateswara Creations | Sri Venkateswara Creations, Sony Pictures India |

| 10 | Sitaare Zameen Par (Stars on Earth) | R.S. Prasanna | India | Sports, Drama | 2.01B | 22.97M | Aamir Khan Productions | Viacom18 |

Production Landscape

The resurgence of Hindi cinema and hope for Indian animation

India continued to be the world’s largest film producer with total theatrical releases reaching 1,572 films in 2025 of which 856 were released in H1 2025 while 716 were released in H2 2025.

A major highlight of H2 2025 was the resurgence of Hindi cinema thanks to the breakout romantic hit Saiyaara (Wandering Star) directed by Mohit Suri and produced by veteran banner Yash Raj Films which released in July and went on to collect a total of INR 3.96 billion (USD 45.26 million) while launching new stars in actress Aneet Padda and actor Ahaan Panday. This was followed by the monstrous success of action blockbuster Dhurandhar (Stalwart) directed by Aditya Dhar and produced by JioStudios which opened in December and became the highest grossing Hindi film of all time at the domestic box office with an India gross of INR 9.50 billion (USD 108.57 million).

Dhurandhar © JioStudios

Overall, 2025 also became the best ever year for Hindi cinema with gross box office collections of INR 55.04 billion (USD 629.0 million), contributing 41% of the year’s total box office figure of INR 133.87 billion (USD 1.53 billion). Unlike recent years when original Hindi films were faltering, in 2025, 93% of Hindi box office collections came from original Hindi language films, with dependence on dubbed South Indian language films dropping from 31% in 2024 to just 7% in 2025.

While Hindi cinema is trying to make a recovery, it remains to be seen if it can sustain the momentum throughout 2026.

Another notable success was seen in Gujarati language cinema with devotional drama Laalo: Krishna Sada Sahaayate (Laalo: Krishna Always Helps) which released in October and became the highest-grossing Gujarati film of all-time collecting INR 1.14 billion (USD 13.0 million). As a result, Gujarati cinema witnessed a staggering 189% growth, rising from INR 0.84 billion (USD 9.6 million) in 2024 to INR 2.42 billion (USD 27.7 million) in 2025.

A standout success in 2025 was homegrown animation hit Mahavatar Narsimha (The Great Incarnation Narsimha), the directorial debut of Ashwin Kumar, which was based on Indian mythology. The Kannada language title—which was dubbed in Hindi and other languages—was produced by well-known banner Hombale Films which also saw another hit in Kantara: Chapter 1. By earning INR 3.01 billion (USD 34.4 million) domestically, Mahavatar Narsimha provided a solid return on investment as it was produced for a relatively modest INR 400 million (USD 4.6 million) and grossed over seven times its budget. It also debunked the myth that Indian animation could not generate mass audience support. The film became the most successful animation release in India beating the previous record holder, the 2019 animation version of The Lion King, which grossed INR 1.88 billion (USD 21.5 million) in India.

Mahavatar Narsimha © Hombale Films

Mahavatar Narsimha © Hombale Films

Financing Models

Equity financing finally catches on

In what is seen as a gradual shift from traditional financing models which are being impacted by theatrical uncertainty and digital disruption, the Indian film industry is finally seeing a gradual increase in equity financing thanks to some high-profile deals in H2 2025, going well into 2026.

In August 2025, the Indian arm of Universal Music and leading banner Maddock Films entered into a strategic partnership for Maddock’s newly formed music label Mad for Mussic which will cover future soundtracks and other offerings. Founded in 2005 by producer Dinesh Vijan and Pooja Vijan, Maddock is best known for its hit horror comedies Stree (2018) and Stree 2 (2024), Bhediya (2022) and Munjya (2024), in addition to one of 2025’s biggest hits, historical epic Chhaava. While investment details were not given, the deal marked the re-entry of Universal Music in Hindi cinema after over two decades. Earlier, in 2022, Nepean Capital acquired equity in Maddock Films for an undisclosed amount.

Universal Music further expanded its reach into Hindi cinema with another agreement announced in early January 2026 in which it acquired a 30% stake in top banner Excel Entertainment in a deal that valued the production house at INR 24 billion (USD 274.3 million). The deal gives Universal worldwide distribution rights for all future original soundtracks created for Excel-backed projects. Excel was founded in 1999 by filmmaker/actor/producer Farhan Akhtar and producer Ritesh Sidhwani and the banner has delivered numerous hits starting with Akhtar’s directorial debut Dil Chahta Hai (2001) and the popular Don franchise, among others.

In December 2025, India’s oldest music label Saregama agreed to invest INR 3.25 billion (USD 37.1 million) in leading banner Bhansali Productions through a multi-stage acquisition that could eventually give it majority control of the studio which was originally founded by well-known film director Sanjay Leela Bhansali in 1996. The studio is known for blockbusters like Hum Dil De Chuke Sanam (1999) and Devdas (2002) among many hits which spawned chart busting soundtracks.

These deals by music majors reflect the historical importance of music in the popularity and commercial appeal of Indian films where hit songs can propel massive monetisation for soundtracks on various distribution platforms.

Overall, equity financing is finally catching on following the ground breaking deal announced by iconic Hindi films banner Dharma Productions in October 2024 when it sold half of its equity to leading industrialist Adar Poonawalla (owner of biotech giant Serum Institute of India) for INR 10 billion (USD 114.3 million) with the balance 50% equity held by Dharma promoter and leading filmmaker Karan Johar. The deal valued Dharma at INR 20 billion (USD 228.6 million).

In February 2026, two more deals were announced which further bolstered equity financing in Indian films, one for boutique banner Sikhya Entertainment and the other for legacy banner Sippy Films. Also announced in February was the launch of Birla Studios, a new venture backed by the Aditya Birla Group conglomerate. We shall look into these deals in detail in the H1 2026 report.

While soft financing is still a way off in India and something that is sorely lacking for independent films, the recent splurge of equity financing still offers hope for the industry as it restructures itself in an increasingly volatile market.

Distribution Climate

Independent films continue to struggle for theatrical distribution

As explained in the report for H1 2025, Indian independent films are now a regular fixture at leading global film festivals but despite the acclaim, they still struggle at home when it comes to theatrical releases. Since the distribution climate is heavily skewered in favour of commercial films coupled with the absence of arthouse cinemas, this makes it difficult for independent films to get adequate screens or show timings.

However, H2 2025 still saw some acclaimed titles getting a theatrical run even if they only managed to attract niche audiences. These included Berlinale title Jugnuma (The Fable) directed by Raam Reddy and Sundance winner Sabar Bonda (Cactus Pears) directed by Rohan Parashuram Kanawade. Following their theatrical run, these titles also locked digital distribution – Jugnuma on Amazon Prime Video and Sabar Bonda on Netflix.

Despite a minority market share, Hollywood films had a good year, collecting a total of INR 14.03 billion (USD 160.3 million), reflecting a strong 49% growth compared to INR 9.41 billion (USD 107.5 million) in 2024. This made 2025 the highest-grossing year for international cinema in India since the pandemic, and the second-best year of all time after 2019. International titles expanded their market share to 10% in 2025 from 8% in 2024, thanks to hits released in H2 2025 like Avatar: Fire and Ash collecting INR 2.39 billion (USD 27.31 million), followed by F1: The Movie at INR 1.26 billion (USD 14.4 million) and Jurassic World: Rebirth at INR 1.25 billion (USD 14.3 million).

Overall, the market share by language continued to be dominated by domestic films at 90% with Hollywood and foreign films only commanding a 10% share. Within domestic films, Hindi cinema commanded a 41% share followed by Telugu cinema at 18% and Tamil cinema at 13% with the balance divided between other languages.

Theatrical Reach

Falling footfalls in an under-screened market

The fact that the world’s most populous country is an under-screened market for cinemas is well known, given that there are currently only 6.8 screens per million, a fall from 7.6 screens in 2018. However, further concern is that footfalls are also declining. According to data from Ormax Media, footfalls declined by 6% to 832 million in 2025 from 883 million in 2024. Separately, a report on the exhibition industry by Ernst and Young indicates that footfalls per screen per year declined by 44%, from 153,000 to 80,000 over the period from 2018–2025. The report surveyed cinemagoers who indicated that one third had reduced the number of films they watched in cinemas since the period before COVID-19. Of India’s population of 1.4 billion, industry estimates suggest that fewer than 150 million (10%) attend cinemas annually, given the availability of alternative viewing options. The report recommends that India’s current screen count of 9,927 should increase to at least 20,000 screens if the government provides incentives like tax holidays, speedy permissions and facilitates financing including foreign direct investment.

Despite falling footfalls and low screen penetration, the report surveyed 14,688 cinemagoers and the results indicated that a majority (81%) preferred going to cinemas rather than watching films on streaming platforms. But 55% of the surveyed cinemagoers also stated that their key concern was the quality of content which has been below expectations. A separate EY survey of content producers indicated that 78% of producers agreed that there was a shortage of quality writers and stories.

As also mentioned in the introduction to this report, a major reason for falling footfalls is attributed to the rise in average ticket prices which have gone up from INR 92 (USD 1.05) in 2015 to INR 161 (USD 1.84) in 2025.

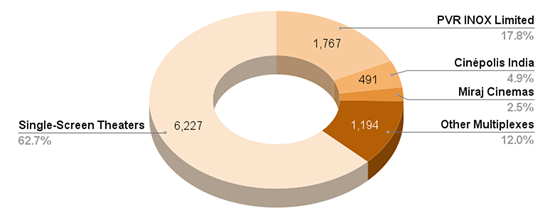

Top Cinema Chains in India (2025)

Source: Multiplex Association of India, Company figures, Industry estimates

Technology and Production Services

The emergence of AI

AI is gaining traction in India and is being deployed in various production activities while AI generated content is also being showcased as the debate over AI’s impact in cinema rages on. In H2 2025, the annual edition of the Indian government’s WAVES Film Bazaar and the International Film Festival of India launched the first-ever AI Film Festival and Cinema AI Hackathon which took place in Goa in November. The festival received a diverse lineup of 68 films, representing 18 countries and also included the Craft Honors which awarded films in various categories.

However, the potential use of AI in mainstream film-making is still a debatable issue. In November 2025, the teaser for Varanasi, the much-anticipated film from iconic director S. S. Rajamouli (known for the Oscar-winning RRR), sparked online chatter questioning if AI was used in the VFX heavy visuals which blended live-action with CGI. Rajamouli dismissed claims that the teaser used generative AI though he did not reject the technology outright and emphasised that AI could serve as a useful tool in the exploratory stages of a film, especially for generating rough ideas.

Taking a larger view, it was the OTT landscape that saw a marked increase in AI-assisted localisation in 2025.

Leading OTT platform JioHotstar became the most aggressive adopter of localized AI tools. In August, it launched the Riya Voice Assistant which uses natural language processing (NLP) to allow users in small towns to search for content in their native dialects. Since sports is the primary content engine for JioHotstar, the platform offers live AI-powered translation of sports commentary into multiple regional languages in real-time. In October, JioHotstar streamed the mythological epic Mahabharat: Ek Dharmayudh (Mahabharat: A War for Righteousness) which is considered India’s first premium series built with a high AI workflow for both visuals and multi-language audio.

Netflix India also enhanced its localisation drive by automating the heavy lifting of regional translation. In its Q4 2025 earnings report, Netflix confirmed it had scaled AI-supported subtitle localisation to handle its massive 2025 content slate, which included over a dozen Indian regional languages. The streamer also beta-tested a GenAI search tool that allows users to explore the catalogue using natural language, significantly reducing the "discovery barrier" for new users in non-metro areas.

Amazon Prime Video expanded its AI-driven voice and image recognition via the Fire TV ecosystem to offer personalized navigation and discovery in regional languages. It also implemented AI-powered streaming protocols to reduce buffering by up to 30%, specifically targeting users on variable 4G/5G networks in smaller towns.

According to industry reports, by the end of 2025, these AI implementations led to a fall in production costs for regional dubbing and subtitling by 25–35%. Localisation that once took weeks was reduced to 48–72 hours.

Streaming Platforms and Digital Growth

Netflix India turns 10 while the digital landscape sees a reset

Netflix India marked its 10th anniversary following its launch in the country in January 2016 which is around the time when India’s streaming market picked up steam. Disney launched its Hotstar service in 2015 (later rebranded as JioHotstar, after Disney India merged with Reliance Industries-backed JioStar) followed by Amazon Prime Video in December 2016. India’s total online audience is estimated at over 600 million users which includes a mix of paid and ad-supported viewership.

Overall, India’s streaming market grew by 9.9% year-on-year in 2025 and while still positive, this marks a "settling" phase compared to the 13–14% growth spurts seen in 2023 and 2024.

As part of this reset phase, there is also a slowing down in the number of originals produced as the market is stabilizing after the overheated growth during the pandemic when OTT consumption skyrocketed. According to an Ormax Media report, the supply of Indian streaming originals continued its downward slide in 2025. After an 18% drop in 2024, the number of original shows across major OTT platforms declined by another 13% in 2025, falling below the 300 mark for the first time since 2020.

Meanwhile, YouTube remains the undisputed champ as India continues to be its biggest market with an estimated 500 million audience, which is double the 254 million users in the US.

When it comes to content, a survey by Ormax Media of 2025’s top 50 streaming shows indicated the year was dominated by returning franchises and established IPs. JioHotstar topped the charts with spy drama Special Ops Season 2 as the most-watched streaming original of the year, amassing 29.6 million viewers followed by the returning season of Criminal Justice: A Family Matter, also on JioHotstar, which garnered 27.7 million viewers. Netflix’s The Ba***ads of Bollywood was the only non-franchise original series amongst the top ten shows, landing at the eighth spot with 16.7 million views. Only two international shows made it to the top 10, both on Netflix – Squid Game Season 3 at the ninth spot with 16.5 million views followed by Stranger Things Season 5 at the tenth spot with 16.4 million. While JioHotstar held the top two spots, Netflix led overall volume with 20 entries in the top 50 shows.

In terms of genres, crime and spy thrillers dominated the rankings followed by reality shows and rural and small-town dramedy shows, most notably Panchayat Season 4 on Amazon Prime Video which attracted 23.8 million viewers.

Top 5 Streamers (2025)

| Rank. | Platform | Paid Subscribers | Market Share (SVOD) | Annual Fee Range (USD) |

|---|---|---|---|---|

| 1 | JioStar (JioHotstar) | ~100M | 31% | 1.00–18.00 |

| 2 | Amazon Prime Video | ~28M | 22% | 12.00–18.00 |

| 3 | Netflix India | ~12M | 16% | 22.00–95.00 |

| 4 | ZEE5 | ~10M | 9% | 6.00–12.00 |

| 5 | SonyLIV | ~8M | 7% | 7.00–14.00 |

Source: Industry estimates

Interview

with Aparna SANYAL, Director, Public Service Broadcast Trust

Within India’s independent scene, documentaries are carving their space despite major obstacles. In recent years, films like All That Breathes by Shaunak Sen and Writing With Fire by Rintu Thomas and Sushmit Ghosh have earned Oscar nominations while documentary short The Elephant Whisperers by Kartiki Gonsalves won an Oscar in 2023. However, India’s documentary ecosystem still needs a major boost, and in this area the New Delhi-based non-profit organisation Public Service Broadcasting Trust has been playing a crucial role since it was established in 2000 as a partnership between public broadcaster Prasar Bharati and the Ford Foundation. In this interaction with PSBT’s recently appointed Director Aparna Sanyal we learn about the challenges and future opportunities for India’s documentary scene.

Q. Following your appointment as director of PSBT from November 2025, could you please share what is the mandate of PSBT going forward and what are the major challenges?

A.

India has a vibrant nonfiction storytelling tradition, but it operates within structural constraints. Unlike fiction, documentaries in India have very limited domestic commissioning avenues, and there are almost no institutional soft funds dedicated exclusively to documentaries.

Our focus is on strengthening the ecosystem for documentaries, and for that our mentoring programme, Doc Commune, launched in 2021–22, works to provide a space to documentary filmmakers to develop their projects over three months. We are seeking to build international pathways to create newer opportunities for filmmakers to connect with the larger global markets, finding international co-producers, and pitching platforms. Commissioning new films remains our primary focus to ensure that there are enough filmmakers who practice the craft. At PSBT, we also have a legacy of domestic documentary filmmaking with 700 films in our library, funded through government grants.

Another challenge is balancing public and artistic value since documentaries have for long been plagued with the challenge of having to speak of ‘public good’. While they will also represent a ‘public good’, we also want to emphasise the creative and artistic potential of documentaries.

We also focus on working with the government for recognition and to build partnerships to impress upon them the importance of the documentary in the creative economy of India.

For us, the major challenges are sustainability and scale. Funding remains fragile and inconsistent. Distribution is fragmented. And there is a growing tension between algorithm-driven content platforms and the slower, research-based practices that documentaries require. The task ahead is to create stability without compromising with the filmmaker’s sensibilities.

Our focus is on strengthening the ecosystem for documentaries, and for that our mentoring programme, Doc Commune, launched in 2021–22, works to provide a space to documentary filmmakers to develop their projects over three months. We are seeking to build international pathways to create newer opportunities for filmmakers to connect with the larger global markets, finding international co-producers, and pitching platforms. Commissioning new films remains our primary focus to ensure that there are enough filmmakers who practice the craft. At PSBT, we also have a legacy of domestic documentary filmmaking with 700 films in our library, funded through government grants.

Another challenge is balancing public and artistic value since documentaries have for long been plagued with the challenge of having to speak of ‘public good’. While they will also represent a ‘public good’, we also want to emphasise the creative and artistic potential of documentaries.

We also focus on working with the government for recognition and to build partnerships to impress upon them the importance of the documentary in the creative economy of India.

For us, the major challenges are sustainability and scale. Funding remains fragile and inconsistent. Distribution is fragmented. And there is a growing tension between algorithm-driven content platforms and the slower, research-based practices that documentaries require. The task ahead is to create stability without compromising with the filmmaker’s sensibilities.

Q. How important is the coproduction model for Indian documentaries especially for raising soft financing since there are hardly any sources for soft financing in India?

A.

Your question contains the answer. Given that we hardly have any sources for soft financing in India, co-productions become inevitable for any documentary that wants to hit the big league.

Given the increasing number of co-productions that are coming together, the challenge is how do we ensure that the co-production process does not become extractive, and creative respect is maintained between the co-producers and the creative teams.

Going forward, I would like to see: Bilateral or multilateral documentary funds between India and key territories (including Asian partners, not just Europe); Simplified co-production treaty mechanisms that explicitly include nonfiction, and find a way around the need for a theatrical release (that remains one of the impediments to using the coproduction treaties for documentaries); Regional South-South collaboration models within Asia, where countries with emerging documentary cultures can share risk and resources; Stronger legal and financial advisory frameworks in India to help filmmakers navigate co-production structures.

If India is to be a meaningful partner in global nonfiction cinema, we need policy recognition of documentary as a cultural sector, not merely a broadcast genre. Hopefully, we’ll get there!

Given the increasing number of co-productions that are coming together, the challenge is how do we ensure that the co-production process does not become extractive, and creative respect is maintained between the co-producers and the creative teams.

Going forward, I would like to see: Bilateral or multilateral documentary funds between India and key territories (including Asian partners, not just Europe); Simplified co-production treaty mechanisms that explicitly include nonfiction, and find a way around the need for a theatrical release (that remains one of the impediments to using the coproduction treaties for documentaries); Regional South-South collaboration models within Asia, where countries with emerging documentary cultures can share risk and resources; Stronger legal and financial advisory frameworks in India to help filmmakers navigate co-production structures.

If India is to be a meaningful partner in global nonfiction cinema, we need policy recognition of documentary as a cultural sector, not merely a broadcast genre. Hopefully, we’ll get there!

Q. The PSBT and the British Council recently launched the Doc Exchange program. Could you share the vision behind this initiative and what you expect to achieve?

A.

Doc Exchange emerged from a clear recognition: Indian documentaries need structured international engagement at the development stage, not just festival exposure at the end stage.

The vision behind Doc Exchange was to build literacy around financing and market opportunities in the UK; Connect emerging filmmakers with UK producers, sales agents and commissioning editors; Encourage long-term partnerships rather than one-off transactions; Situate documentary within the broader creative economy ties between India and the UK.

In many ways, Doc Exchange is an extension of what we do at PSBT through Doc Commune which is to strengthen projects at the conceptual level before they enter the marketplace. But this platform adds a strategic international dimension.

The vision behind Doc Exchange was to build literacy around financing and market opportunities in the UK; Connect emerging filmmakers with UK producers, sales agents and commissioning editors; Encourage long-term partnerships rather than one-off transactions; Situate documentary within the broader creative economy ties between India and the UK.

In many ways, Doc Exchange is an extension of what we do at PSBT through Doc Commune which is to strengthen projects at the conceptual level before they enter the marketplace. But this platform adds a strategic international dimension.

Nyay BHUSHAN

Producer, Photographer

Nyay Bhushan is founder of Connectment Films under which he has produced and directed short films Backdrop, The Saint, Stuck in Inner Traffic and Mango Shake which were featured on digital platform Filmaka. Connectment is currently developing various feature projects as co-productions. In the Nineties, Nyay co-founded CONNECT, India’s first magazine on global entertainment, which received a message from Steven Spielberg for its readers. Nyay served as the first India-based regular correspondent for Billboard (1997–2008) and The Hollywood Reporter (1999–2020). As a fine art photographer, his work has received several honours at the International Photography Awards and the Prix de la Photographie Paris (PX3) Awards.

Source: Ormax Media Box Office Report 2025