Title

THE A REPORT

2025 H2

Vorakorn RUETAIVANICHKUL

Author, Filmmaker &

Vorakorn RUETAIVANICHKUL

Author, Filmmaker & Researcher

Griffith Film School of Griffith University

Updated on 12 May 2026

Death Whisperer 3

Death Whisperer 3© M Studio

Overview

The Great Market Correction

The second half of 2025 cemented the Thai theatrical market as a highly polarized, "blockbuster-or-bust" ecosystem. Critics defined H2 2025 by a harsh reality: "Quantity over Quality." While theaters were flooded with new local titles weekly, overall profitability plummeted due to supply overload and audience fatigue.

A rigorous dissection of the box office exposes the sheer brutality of this market correction. Thai films secured a formidable 34.6% market share within the Overall Top 10 (THB 787.08 million / USD 23.61 million), yet this figure masks a stark domestic monopoly. The supernatural tentpole Death Whisperer 3 (THB 465 million / USD 13.95 million) single-handedly carried 46.6% of the entire local Top 10 revenue. When joined by the only other standout performers—Our House (THB 130 million / USD 3.90 million), 4 Tigers (THB 102.08 million / USD 3.06 million), and Kayaor (THB 90 million / USD 2.70 million)—this elite quartet monopolized 79% of domestic earnings. Beyond this upper echelon, the drop-off was catastrophic. Mid-tier franchise extensions and legacy slapstick comedies languished in the dismal THB 24 million–63 million (USD 0.72 million–USD 1.89 million) range. This mathematical polarization proves unequivocally that the "middle class" of Thai cinema has evaporated; audiences are reserving their capital strictly for premium experiences, officially killing the industry's "Factory Mode" of churning out fast content.

4 Tigers © Sahamongkol Film International

Furthermore, a seismic demographic shift emerged globally, as Japanese animation demonstrated definitive dominance over traditional American franchises. Demon Slayer: Kimetsu no Yaiba - Infinity Castle (THB 309.3 million / USD 9.28 million) outperformed legacy Hollywood live-action reboots like Jurassic World: Rebirth (THB 289.3 million / USD 8.68 million) and Superman (THB 88.4 million / USD 2.65 million), signaling a permanent change in theatrical event preferences.

Compounding this market volatility was a major political shift that effectively brought the government-backed Thailand Creative Culture Agency (THACCA) initiative to a halt. This abrupt change has created a critical policy vacuum, leaving the future of state funding for independent cinema highly uncertain as the industry heads into 2026.

Despite domestic theatrical turbulence, the broader ecosystem demonstrated remarkable adaptive resilience. Driven by a newly enforced 30% cash rebate, inbound international productions generated a record-breaking THB 7.71 billion (USD 231.32 million), effectively becoming the industry's financial backbone. Simultaneously, major local players pursued bold global expansion, successfully transitioning Thai horror into a bankable "Global Export IP". In the digital realm, while local telecom-backed streamers maintained strict viewership dominance, global giants like Netflix pivoted to financing high-end "Local Originals" to capture distinct audience segments.

Consequently, H2 2025 marked a structural evolution: the Thai film industry is no longer relying solely on domestic box office luck, but actively re-engineering itself into a resilient, transnational content hub.

Consequently, H2 2025 marked a structural evolution: the Thai film industry is no longer relying solely on domestic box office luck, but actively re-engineering itself into a resilient, transnational content hub.

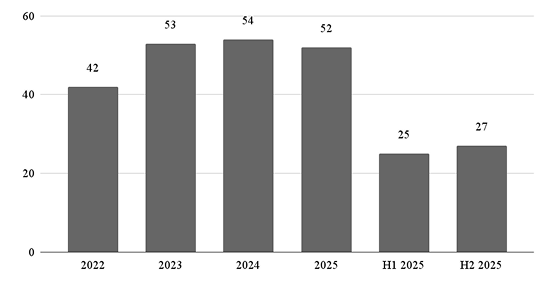

Figures of Released Domestic Feature (2022-2025)

Top 10 Films in Thailand Box Office (H2 2025)

You can scroll left and right to view the content.

| No | Title | Director | Country | Genre | Gross (THB) |

Gross (USD) |

Production Company |

Distribution Company |

|---|---|---|---|---|---|---|---|---|

| 1 | Avatar: Fire and Ash | James Cameron | USA | Sci-Fi, Action | 512.83M | 15.39M | Lightstorm Entertainment, 20th Century Studios | 20th Century Studios |

| 2 | Death Whisperer 3 | Narit Yuvaboon, Thanadet Tom Pradit | Thailand | Supernatural Horror | 465M | 13.95M | Major Join Film, BEC World | M Studio |

| 3 | Demon Slayer: Kimetsu no Yaiba - Infinity Castle | Haruo Sotozaki | Japan | Animation, Action | 309.3M | 9.28M | Ufotable | Aniplex, Toho (Japan), Crunchyroll, Sony Pictures Releasing (Worldwide) |

| 4 | Jurassic World: Rebirth | Gareth Edwards | USA | Action, Adventure | 289.3M | 8.68M | Universal Pictures, Amblin Entertainment | Universal Pictures |

| 5 | Zootopia 2 | Jared Bush, Byron Howard | USA | Animation, Comedy | 204.26M | 6.13M | Walt Disney Animation Studios | Walt Disney Studios Motion Pictures |

| 6 | Our House | Kongkiat Komesiri | Thailand | Horror, Thriller | 130M | 3.9M | Ghost Light, Shinesaeng Ad.Venture | Shinesaeng Ad.Venture |

| 7 | 4 Tigers | Kongkiat Komesiri | Thailand | Action, Fantasy | 102.08M | 3.06M | Sahamongkolfilm International, Kongkiat Production | Sahamongkolfilm International |

| 8 | Kayaor: Disrespecting Faith and the Supernatural | Pawat Panangkasiri | Thailand | Supernatural Horror, Drama | 90M | 2.7M | M Studio, Sao Noi Phet Ban Phaeng, Phawat Film 45 | M Studio |

| 9 | Superman | James Gunn | USA | Superhero, Action | 88.4M | 2.65M | DC Studios, The Safran Company, Troll Court Entertainment | Warner Bros. Pictures |

| 10 | F1: The Movie | Joseph Kosinski | USA | Action, Drama | 86M | 2.58M | Apple Studios, Jerry Bruckheimer Films, Plan B Entertainment, Dawn Apollo Films | Warner Bros. Pictures, Apple Original Films |

Top 10 Domestic Films in Thailand Box Office (H2 2025)

You can scroll left and right to view the content.

| No | Title | Director | Country | Genre | Gross (THB) |

Gross (USD) |

Production Company |

Distribution Company |

|---|---|---|---|---|---|---|---|---|

| 1 | Death Whisperer 3 | Narit Yuvaboon, Thanadet Tom Pradit | Thailand | Supernatural Horror | 465M | 13.95M | Major Join Film, BEC World | M Studio |

| 2 | Our House | Kongkiat Komesiri | Thailand | Horror, Thriller | 130M | 3.9M | Ghost Light, Shinesaeng Ad.Venture | Shinesaeng Ad.Venture |

| 3 | 4 Tigers | Kongkiat Komesiri | Thailand | Action, Fantasy, Crime | 102.08M | 3.06M | Sahamongkolfilm International, Kongkiat Production | Sahamongkolfilm International |

| 4 | Kayaor: Disrespecting Faith and the Supernatural | Pawat Panangkasiri | Thailand | Supernatural Horror, Drama | 90M | 2.7M | M Studio, Sao Noi Phet Ban Phaeng, Phawat Film 45 | M Studio |

| 5 | Nak Loves Mak Sooo Much! | Choosak Iamsuk | Thailand | Comedy, Rom-Com, Horror | 63.5M | 1.91M | Black Dragon Entertainment, Transformation Films, Nation Group, Bangfire Film | Black Dragon Entertainment |

| 6 | My Boo 2 | Komgrit Triwimol | Thailand | Rom-Com, Horror, Fantasy | 34.13M | 1.02M | Jungka Studio, Karmanline, M Studio | M Studio |

| 7 | Tha Rae: The Exorcist | Taweewat Wantha | Thailand | Supernatural Horror, Action, Thriller | 34M | 1.02M | Sahamongkol Film International | Sahamongkol Film International |

| 8 | Hor Taew Tak: Haek Lee Hu | Poj Arnon | Thailand | Slapstick, Satire, Horror Comedy | 27.88M | 0.84M | M Studio, Mono Original, Film Guru | M Studio |

| 9 | The Last Shot | Puttipong Nakthong | Thailand | Action, Crime, Drama | 25.7M | 0.77M | M Studio, Plan B Media | M Studio |

| 10 | Khok Kalok Village | Poj Arnon | Thailand | Comedy, Horror | 24.58M | 0.74M | Mono Original, M Studio, Film Guru | M Studio |

- Average ticket price: approx. THB 293 (≈ USD 9.2, at 1 USD = 32 THB)

Notes:

- USD conversion is an estimate based on an exchange rate of ~33.33 THB to 1 USD

- The box-office statistics for each film are collected from the weekly box office report. The data is accurate as of February 28, 2026, and sourced from ThailandBoxOffice.com, which is the only provider of nationwide box office estimates and an affiliate of Major Cineplex Group, the largest multiplex chain in Thailand

- The final adjustment for Death Whisperer 3, Our House, and 4 Tigers are sourced from the result of Thailand Box Office Awards 2025

Notes:

- USD conversion is an estimate based on an exchange rate of ~33.33 THB to 1 USD

- The box-office statistics for each film are collected from the weekly box office report. The data is accurate as of February 28, 2026, and sourced from ThailandBoxOffice.com, which is the only provider of nationwide box office estimates and an affiliate of Major Cineplex Group, the largest multiplex chain in Thailand

- The final adjustment for Death Whisperer 3, Our House, and 4 Tigers are sourced from the result of Thailand Box Office Awards 2025

Production Landscape

The Demise of the Formula and the Rise of Craft

H2 2025 did not just disrupt the production landscape; it dismantled the industry's most sacred cash cows. For years, Thai studios rested comfortably on the "guaranteed formula" of low-budget horror-comedies and rushed sequels for quick returns. But the second half of the year delivered a harsh awakening: brand recognition is no longer a safety net for a hollow script. The most spectacular casualty of this shift was My Boo 2 (THB 34.13 million / USD 1.02 million). Despite returning its original cast and director, the highly anticipated sequel crashed and burned, a victim of industry complacency. Audiences, armed with the rapid-fire power of social media word-of-mouth, penalized films they perceived as rushed or riddled with plot holes. Consequently, the once-lucrative comedy-horror genre flatlined in the THB 20–30 million (USD 0.60 million–USD 0.90 million) purgatory.

From the ashes of these formulaic failures rose a new era of "Cinematic Supernaturalism," fueled by meticulous craftsmanship rather than cheap thrills. The undisputed dark horse of this movement was Kongkiat Komesiri’s Our House. Shunning heavy marketing campaigns, this standalone psychological horror relied entirely on the gravitational pull of a rock-solid screenplay. It generated a relentless, sleeper-hit momentum, ultimately over-performing expectations to amass a staggering THB 130 million (USD 3.90 million). Komesiri continued his reign over the action-fantasy space with 4 Tigers (THB 102.08 million / USD 3.06 million), proving definitively that the modern Thai audience hungers for high-production-value, serious storytelling that breathes life into local mysticism.

Beyond the commercial battlefield, the independent sector birthed what was arguably the most critically profound film of the year: Ratchapoom Boonbunchachoke’s A Useful Ghost by 185 Films. Anchored by the delightfully bizarre premise of a "vacuum cleaner ghost," the film operated as a sharp, socio-political allegory. Unsurprisingly, this esoteric narrative struggled to find a foothold among mainstream domestic audiences conditioned for straightforward scares, bowing out of theaters quietly with a modest THB 2.88 million (USD 0.09 million).

This muted domestic reception stood in stark contrast to its monumental global triumph earlier in the year. A Useful Ghost had already shattered a decades-long dry spell by capturing the prestigious Grand Prize at the Cannes Film Festival's Critics' Week, making it the undeniable choice for Thailand’s official submission to the 98th Academy Awards. However, this historic momentum was derailed by a shocking administrative failure by the National Federation of Motion Pictures and Contents Associations (MPC), where the film was disqualified due to mishandled paperwork and missed deadlines, resulting in an "Empty Seat" for Thailand at the Oscars. This bureaucratic blunder ignited a firestorm of industry outrage, exposing deep rot in the establishment's back-office operations and robbing Thai cinema of a well-deserved moment in the global spotlight.

Shell-shocked by the crisis of faith in 2025, major studios are now forced to execute a swift pivot from "Quantity" to "Craftsmanship." The upcoming 2026 slates reflect a radically altered industry standard, one that heavily prioritizes extended, rigorous pre-production. The "Script Doctor" has evolved from a luxury to an absolute necessity, deployed to seal narrative leaks long before a single frame is shot. Furthermore, the hubris of intuition-based releasing is dead. Studios are now subjecting their films to brutal "Test Screenings," demonstrating a newfound, humble willingness to order costly reshoots if early audience feedback signals danger. For the Thai filmmaker, the battlefield has expanded; they are no longer just fighting Hollywood blockbusters, but the dopamine-driven, algorithmic supremacy of TikTok and Netflix. Survival now demands absolute "Audience Supremacy."

Financing Models

Strategic Syndication and Corporate Capital

The financing ecosystem in H2 2025 has shifted away from the traditional sole-investor studio model toward highly syndicated, multi-partner Joint Ventures (JVs). This strategy is designed to de-risk theatrical investments while maximizing cross-media marketing synergy.

The prime architect of this shift is M Studio, which revealed a vast 17-film slate for 2026 entirely built on collaborative funding. By executing a strategic rollout, their local supremacy generated THB 555 million (USD 16.65 million) across their top releases in H2 2025. This dominance is underpinned by a multi-pronged financing strategy that begins with aggressive broadcaster syndication. By partnering directly with dominant television and media networks such as BEC World (Channel 3), Media Studio (Channel 7), MONO Original, and Workpoint (Karman Line), M Studio secures substantial "free" marketing airtime and guarantees a lucrative secondary broadcast window.

Beyond traditional media, these joint ventures are actively integrating subcultures and niche intellectual properties to guarantee a box office floor. By co-financing films alongside established giants like The Ghost Radio (Thailand's largest horror storytelling IP) and Be On Cloud (a powerhouse in Boys' Love/Y-series), studios ensure that a highly dedicated fan base is mobilized on opening weekend. A prime example of this hyper-localized strategy was the supernatural drama Kayaor: Disrespecting Faith and the Supernatural (THB 90 million / USD 2.70 million). Co-financed by M Studio and the premier "Mor Lam" (traditional Northeastern Thai musical) troupe Sao Noi Phet Ban Phaeng, the production weaponized the immense regional magnetism of its musical cast. By directly targeting the fiercely loyal Northeastern (Isan) demographic, the film successfully bypassed traditional marketing hurdles and secured a highly lucrative, built-in audience.

Kayaor: Disrespecting Faith and the Supernatural

Kayaor: Disrespecting Faith and the Supernatural © M Studio

Furthermore, H2 2025 witnessed a significant influx of corporate "hard money," marking the visible entry of non-entertainment capital into film financing. Heavyweight out-of-home media giants like Plan B Media, media buying agencies such as MI Group, and even cryptocurrency and tech unicorns like Bitkub are now actively co-financing feature films. This unprecedented influx signals that private equity and corporate conglomerates increasingly view local cinema not merely as entertainment, but as a high-yield alternative asset class and a potent branding vehicle.

Conversely, the independent sector relies heavily on a patchwork of "soft money," a landscape severely disrupted in H2 2025 by a major political shift. Regarding the current status of the Thailand Creative Culture Agency (THACCA), it is crucial to clarify that the entity has not been "dissolved" in the sense of a permanent agency shutting down, as it had not yet attained formal, independent legal status. Instead, what has effectively ceased to exist is the National Soft Power Strategy Committee—the governing body responsible for driving the THACCA initiative and overseeing its institutionalization. In its initial phase, THACCA functioned strictly as a High-Level Coordinating Committee. Its primary mandate was to serve as a centralized hub, aligning the objectives of various ministries—such as the Ministry of Culture and the Ministry of Tourism and Sports—to synergize their respective budgets for joint creative projects.

Following the administrative transition from the Phuethai Party to the Bhumjaithai Party’s leadership, the terms of these specialized sub-committees, composed of industry experts and private sector representatives, expired and were not renewed. Consequently, the legislative process to institutionalize THACCA into a permanent, autonomous government agency via the Creative Culture Promotion Act has been halted. As a result, the centralized "Soft Power" budget has reverted to the control of individual bureaucratic silos. For the film industry, this means the streamlined, committee-led approach to international co-production and festival support has regressed to a more fragmented, ministry-by-ministry administrative model.

Fortunately, the industry has not faced a complete standstill. The 220 million THB (USD 6.60 million) budget previously approved in H1 for 88 projects spanning films, TV series, Documentaries, Animation, and Shorts—including highly anticipated works from renowned auteurs—remains legally secured. These projects are currently in production and will continue to be completed and rolled out over the next 1-2 years. However, a looming challenge remains: the new administration has shown no intention of reviving THACCA's initiatives, creating a critical policy vacuum. This regression leaves independent financing exceptionally fragile and casts a long shadow of uncertainty over the future of state-backed funding beyond 2026.

Distribution Climate

Domestic Duopolies and Global Export Triumphs

Thailand’s distribution and exhibition climate operates as a highly consolidated, vertically integrated near-duopoly. The market is overwhelmingly controlled by two major exhibition chains: Major Cineplex and SF Cinema.

This vertical integration dictates the distribution climate. Major Cineplex’s production and distribution arm, M Studio, essentially acts as the primary gatekeeper for local content. Films produced or co-financed under their umbrella benefit from preferential screen allocations, prime showtimes, and extensive in-theater marketing. For independent producers and smaller distributors, penetrating this closed ecosystem remains the most significant barrier to entry, as un-affiliated films are often relegated to off-peak hours or pulled from theaters abruptly if opening day numbers are soft.

While maintaining an iron grip on the domestic market, M Studio simultaneously orchestrated a historic outbound distribution victory in H2 2025. Executing a global sales strategy initiated at the European Film Market (EFM) earlier in the year, their supernatural tentpole Death Whisperer 3 shattered international franchise records. According to Screen Daily (September 2025), M Studio successfully secured comprehensive distribution rights spanning North America and Latin America, while closing specific territorial partnerships for Australia/New Zealand (via Little Monster), India and Pakistan (via FearFolks), and Russia/CIS (via Carte Color). This landmark achievement effectively transitions Thai horror from a regional niche into a highly bankable "Global Export IP," proving that local vertically integrated studios can now successfully operate on the world stage.

Regarding international content, major Hollywood studio films are distributed by their respective local branches (e.g., Warner Bros. Pictures, Disney), though they must still negotiate revenue terms with the dominant exhibition duopoly. Conversely, independent foreign films from Europe, the US, and Asia are handled by specialized local distributors like Sahamongkol Film International (Mongkol Major), HAL Distribution, and the rapidly expanding Shinesaeng Ad.Venture.

A defining market shift in H2 2025 was the rapid rise of anime distributors, successfully challenging the traditional Hollywood hierarchy. Companies like Sony/Aniplex and Crunchyroll proved they could command saturation-level screen counts previously reserved only for major US tentpoles. The results were staggering: Demon Slayer: Kimetsu no Yaiba - Infinity Castle secured the 3rd spot overall with THB 309.3 million (USD 9.28 million), single-handedly generating a 13.6% market share among the top tier. By out-earning highly anticipated Western IP reboots such as Universal's Jurassic World: Rebirth (THB 289.3 million / USD 8.68 million) and Warner Bros.' Superman (THB 88.4 million / USD 2.65 million), anime distributors have confirmed a permanent demographic shift. Thai audiences are now demonstrably prioritizing premium Japanese animated events over standard Hollywood superhero or action fare, forcing local exhibitors to reallocate prime showtimes accordingly. This performance is particularly notable given that Demon Slayer's revenue was generated heavily from premium localized merchandising bundles ("Fan Screenings"), pushing its Revenue-Per-Seat far above the Hollywood average.

Theatrical Reach

Premium Monetization and the Fandom Economy

Demon Slayer: Kimetsu no Yaiba - Infinity Castle © Sony Pictures Releasing

In H2 2025, Thai exhibitors officially abandoned the race for maximum admissions, pivoting instead to a strategy of maximizing revenue per capita. This shift proved highly resilient, as evidenced by the market leader Major Cineplex's 2025 report; despite a 2% drop in total revenue (heavily driven by a 19% decline in traditional cinema advertising), the company’s operating profit surged by 10% to THB 736 million (USD 22.08 million). This profitability was engineered by deliberately reducing heavy ticket discounting and funneling audiences toward premium, high-margin experiences. Driven by visually spectacular event films like James Cameron’s Avatar: Fire and Ash, Apple’s F1: The Movie, and the local phenomenon Death Whisperer 3, demand for premium large-format (PLF) screens reached an all-time high, prompting rival SF Cinema to standardize "All RGB Laser" projectors across both its urban hubs and newly launched provincial branches.

Top 5 Streamers

You can scroll left and right to view the content.

| Name | Number of Screens | Market Share | |

|---|---|---|---|

| 1 | Major Cineplex | 854 | 80% |

| 2 | SF Cinema | 400 | 15% |

| Others | ~5% |

Reference (data based on different timeframes; indicative only):

- Major Cineplex, One Report, 2025

- Money & Banking, article on SF Corporation, 2023

- The Matter, How Cinema Survive After Lift the Lockdown, 2021

- Major Cineplex, One Report, 2025

- Money & Banking, article on SF Corporation, 2023

- The Matter, How Cinema Survive After Lift the Lockdown, 2021

Recognizing the inherent volatility of traditional box office returns, exhibitors executed a masterclass in monetizing the "Fandom Economy." SF Cinema, in particular, transformed its auditoriums into high-margin concert venues via the "SF MUSIC IN CINEMA" initiative. They successfully hosted the "HYBE CINE FEST IN ASIA"—featuring concert films of global K-Pop giants and introducing in-theater karaoke ("Cinema Noraebang")—and screened a sold-out live concert of Thai soul band The Parkinson in Dolby Atmos. Most ingeniously, exhibitors weaponized dedicated Boys' Love (BL) fandoms to drive Hollywood ticket sales, hosting exclusive "Friends Screenings" of Avatar featuring top-tier BL actors to guarantee sold-out auditoriums at premium prices through localized fan loyalty.

Beyond the silver screen, the duopoly diversified their geographic and retail footprints to insulate against future shocks. Major Cineplex boldly divested its underperforming Cambodian operations to fund a strategic 26-branch expansion into Thailand’s secondary provinces, targeting regional demographics less saturated by global streaming subscriptions. Simultaneously, both chains evolved their concessions into retail Fast-Moving Consumer Goods (FMCG). While Major Cineplex formed a joint venture with seaweed giant Taokaenoi to distribute "Major Popcorn" in mass retail, SF Cinema pursued the boutique lifestyle market, partnering with premium mineral water 6ty Degrees and cult-favorite dessert brand SOURI for cross-branded treats. This evolution from basic theater snacks to premium lifestyle products successfully cemented the cinema as a holistic, high-spending entertainment destination.

Technology and Production Services

Script Incubation and the Inbound Boom

In H2 2025, the definition of "production technology" in Thailand expanded significantly beyond physical hardware and VFX capabilities, shifting toward robust "Development and Pre-production Infrastructure." While high-end Virtual Production (LED volume stages) remains largely monopolized by commercial advertising shoots and large-scale inbound productions servicing Hollywood, the local domestic film sector fundamentally re-engineered its approach to production services. For instance, the highly publicized THB 193 million (USD 5.79 million) Figment Studio—launched earlier in the year as a revolutionary tool for Thai cinema—has effectively become an exclusive playground for foreign mega-shoots and well-funded streamers. Local studios, grappling with budget constraints and the "Quality Crisis," simply cannot afford these premium rates.

Simultaneously, the physical production service sector remains a vital economic pillar. In fact, inbound foreign shoots proved to be the industry's financial backbone in 2025. According to the Department of Tourism (DOT), the year culminated as a "Golden Year", propelled by the newly enforced 30% cash rebate. While the "Set-Jetting" boom was ignited by the global releases of Jurassic World: Rebirth and The White Lotus S3 earlier in the year, the momentum carried powerfully into H2. A prime catalyst was the August 2025 premiere of FX's Alien: Earth; its showcase of Thailand as a futuristic battleground drove The Studio Park bookings for the remainder of the year, filling the facility's pipeline even after the main unit had wrapped. Consequently, October 2025 set a historic record with THB 2.58 billion (USD 77.41 million) in monthly investment, driven largely by the massive unit of the Bollywood spy-universe juggernaut Dhurandhar (starring Ranveer Singh). The production utilized Bangkok to recreate complex international conflict zones, wrapping principal photography just as the fiscal year closed. The year-end total reached a staggering 546 foreign productions, generating over THB 7.71 billion (USD 231.32 million) in direct revenue—an amount nearly 3.4 times the total earnings of the entire Top 10 national box office.

Dhurandhar

Dhurandhar © Jio Studios

Streaming Platforms and Digital Growth

Local Telcos vs. Global Originals

The streaming landscape in Thailand presents a unique anomaly compared to global trends: the undeniable dominance of local telecommunications conglomerates over international streaming giants. According to the ADTEB Cross-Platform Ratings from October 2025, localized platforms greatly outperformed global competitors in terms of cumulative unique viewership. TrueID led the market significantly with a reach of 12,879,237 viewers, followed by AIS Play with 6,420,543. The global giant Netflix secured third place with 6,107,238 viewers, while regional players WeTV and MONOMAX had 3,239,899 and 2,059,836 viewers, respectively.

This localized dominance is engineered through strategic "bundling" strategies. TrueID and AIS Play leverage their vast mobile subscriber bases by integrating OTT access directly into affordable cellular data packages (ranging from USD 2 to 5). Consequently, these platforms have become the primary digital consumption hubs for the masses, particularly for acquiring live sports, localized dubs of Asian dramas, and exclusive domestic TV content.

For local film producers, the OTT sector has firmly solidified its role as a crucial secondary recoupment window, especially in the wake of the H2 2025 box office volatility. Mid-tier productions and comedies that underperformed or were swiftly pulled from theaters during the "supply overload"—such as My Boo 2—heavily relied on streaming acquisitions to break even.

Meanwhile, global platforms like Netflix have shifted their strategy away from acquiring high volumes of theatrical run-offs. Instead, they are heavily investing in commissioning high-budget "Local Originals," effectively acting as deep-pocketed studio financiers. In H2 2025, this strategy yielded spectacular results through a "Twin Towers" approach, carried by two distinct blockbuster titles: the cinematic film Tee Yai: Born to Be Bad and the episodic series The Believers 2. These titles perfectly illustrated Netflix's dual-pronged dominance in targeting different market segments.

Tee Yai: Born to Be Bad (released November 13) served as the platform's global breakout. The 1980s period action film by the veteran Nonzee Nimibutr, heavily praised for its visceral long-take action sequences starring Apo Nattawin, successfully transcended cultural barriers. It debuted at #1 in Thailand and rapidly pierced the Global Top 10 Non-English Movies chart, peaking at #6 with a confirmed 2.4 million views in its first week. Conversely, the 8-episode series The Believers 2 (released December 4) acted as the domestic juggernaut. While its deep dive into the complex morality of "commercialized Buddhism" proved too culturally specific for global audiences—failing to chart in the Global Top 10—it generated unparalleled social impact within Thailand. It dominated the #1 spot on Netflix Thailand's TV chart for weeks and consistently topped X trends, sparking nationwide debates on religious institutions. Together, this comparative success proves that Netflix has successfully mastered both international reach via high-octane action and profound domestic cultural engagement via dark, localized drama, solidifying streaming as a primary destination for premium Thai storytelling.

Top 5 Streamers (H2 2025)

You can scroll left and right to view the content.

| No | Name | Monthly Cumulative Reach | Subscription Fee Range |

|---|---|---|---|

| 1 | True ID | 12,879,237 | USD 2–4 |

| 2 | AIS Play | 6,420,543 | USD 5–31 |

| 3 | Netflix | 6,107,238 | USD 3–13 |

| 4 | We TV | 3,239,899 | USD 4 |

| 5 | MONOMAX | 2,059,836 | USD 3–9 |

International Co-Production

The Outbound Shift and Pan-Asian Alliances

Historically, Thailand's international film strategy leaned heavily toward servicing inbound foreign shoots rather than initiating outbound intellectual properties. However, H2 2025 marked a definitive structural shift as the independent commercial sector began constructing its own international co-production infrastructure to bypass domestic market limitations.

The most prominent example of this evolution is the launch of Common Ground, a new business unit established by independent distributor and producer Shinesaeng Ad.Venture (the studio behind the H2 sleeper hit Our House). Rather than operating as a traditional studio, Common Ground is explicitly engineered as a "Co-Production Hub." It functions as an incubator that bridges local creators with strategic partners for cross-border investment, production, and distribution. Leveraging the THB 130 million (USD 3.90 million) financial success of Our House, Shinesaeng Ad.Venture immediately reinvested its capital into infrastructure, announcing an extensive 2026–2027 slate, including the action-drama Prasert (with Kongkiat Production) and the supernatural thriller No Caller ID (with Strippers Films).

Crucially, this initiative is inherently outbound. Executives from Common Ground and Shinesaeng Ad.Venture actively positioned these new co-productions at the Hong Kong International Film & TV Market (FILMART) in March 2026, pitching Thai IP directly to Asian investors. This signals a profound maturation in the private sector: mid-tier studios are no longer waiting for unpredictable state grants or domestic box office luck. Instead, they are building their own strategic "Asian Alliances," solidifying Thailand's status not just as a filming location, but as a formidable creator of exportable, pan-Asian cinematic content.

Prasert

Prasert © Shinesaeng Ad.Venture

Conclusion

The Purge and the Transnational Re-engineering

To reflect on H2 2025 is to witness not merely a maturation, but a ruthless and necessary purge of the Thai film industry. The era of complacent, factory-line filmmaking was decisively incinerated by a domestic audience that now demands absolute craftsmanship. Yet, from the ashes of this volatility emerged a hardened structural resilience. The political vacuum left by the disruption of THACCA initiative did not paralyze the industry; instead, it forced independent studios to claim their sovereignty, bypassing state reliance to forge robust pan-Asian alliances. Simultaneously, corporate titans transformed local horror and action into highly lucrative, borderless IP. Bolstered by a multi-billion-baht inbound production engine, Thailand has officially shed its legacy as a passive filming backdrop. As we look to 2026, the Thai film industry stands completely re-engineered—uncompromising, fiercely strategic, and commanding its own narrative on the global stage. The future of this market no longer belongs to those who chase the trends; it belongs exclusively to the architects who build them.

Vorakorn RUETAIVANICHKUL

Author, Filmmaker & Researcher/ Griffith Film School of Griffith University

Vorakorn 'billyv◊rr' Ruetaivanichkul is a Thai author, filmmaker, and Australia Awards for ASEAN scholar operating across regional independent cinema and major international productions such as Ron Howard’s Thirteen Lives (2022). As a 2024 ArtsEquator Fellow, he pioneered the critical framework of 'Mek◊ng Sci-Fi'—a foundation that now heavily informs his overarching narrative universe, 'Fut◊rity'. Currently pursuing his PhD at Griffith Film School, Vorakorn is exploring AI-assisted frameworks for long-form narrative development. Driven by a deep commitment to synthesizing emerging technology with regional aesthetics, his mission is to empower creators of the Global South to cultivate their own distinct narrative voices and creative independence. Follow his journey at www.billyvorr.com.

Source:

- - https://www.facebook.com/BangkokCritics

- - https://marketeeronline.co/archives/396811

- - https://investor.majorcineplex.com/th/downloads/one-reports

- - https://en.moneyandbanking.co.th/2023/41342/

- - https://thematter.co/social/how-cinema-survive-after-lift-the-lockdown/157

- - https://image.makewebcdn.com/makeweb/0/2CAT32K6W/Document/ADTEB_report_OCT_25.pdf?v=20240291424#page=28.00

- Bangkok Critics Assembly (Facebook), H2 domestic figures, supplemented with arthouse titles (limited release)

- Marketeer Online, The Golden Year of Thai Film, 2024